The 2026 Federal Budget measures have been a prominent topic of conversation in recent weeks. Many clients have been questioning how the proposed changes may impact their individual circumstances. While these measures are yet to be legislated, the level of uncertainty has prompted discussions, although our key message is – remain cautious and don’t act until legislation is passed unless you are considering a new transaction.

In this article, we outline the key changes to consider and what your next steps may be if any of the below measures apply to you:

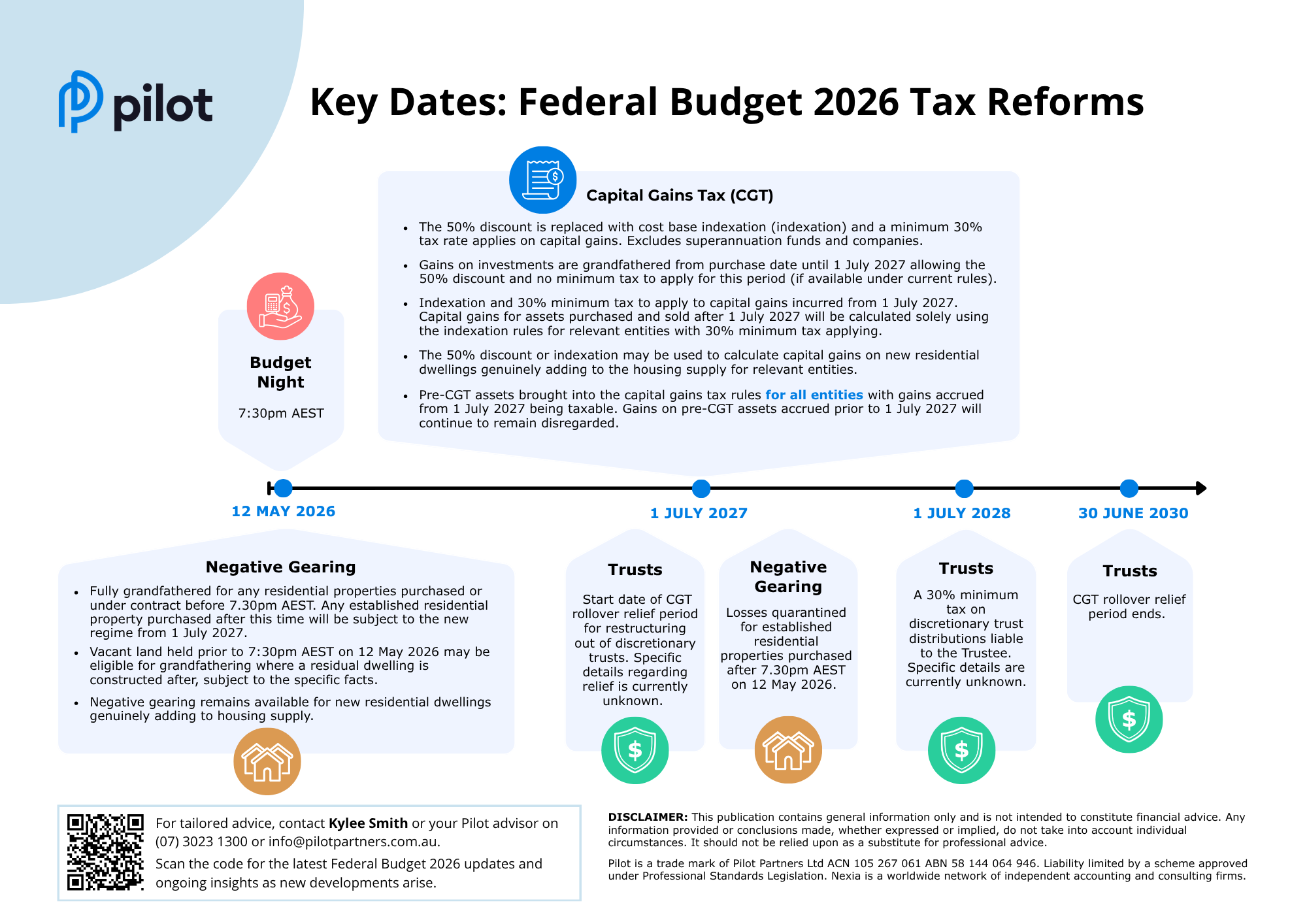

Additionally, our infographic covers the expected timeline for these key Federal Budget tax reforms.

Capital Gains Tax changes: Key rules, rates and what investors need to know

Proposed CGT changes: What the draft legislation says

On 28 May 2026 the Government introduced draft legislation to implement capital gains tax and negative gearing reform. The proposed changes to CGT will see the after-tax return on investment assets change significantly. Many taxpayers will likely see their after-tax return decrease with the proposed changes, specifically given the introduction of a minimum 30% tax on any capital gains.

New cost base indexation rules from 1 July 2027

Cost base indexation will be available to Australian resident individuals or trusts (including individuals and trusts that are partners in partnership) on capital gains arising on or after 1 July 2027. Eligibility for indexation will require the relevant capital asset to have been held for a minimum period of 12 months.

The draft legislation provides guidance on how assets held prior to 1 July 2027 will be treated for tax purposes as they transition from either the 50% CGT discount regime or pre CGT status to the cost base indexation method. Importantly, the new indexation method will not apply to superannuation funds or companies. Although, if a company or superannuation fund owns a pre-CGT asset, this asset will be brought into the tax system – based on the draft legislation – from 1 July 2027.

Broadly, all existing CGT assets will be deemed to be disposed of on 30 June 2027 and immediately re‑acquired on 1 July 2027 (this is known as the deemed disposal). The gain or loss made for the period ending 30 June 2027 will have access to the 50% discount and pre-CGT status (subject to current legislation exclusions). Although there is a deemed sale to move to the new rules, the original acquisition date of the asset will remain relevant for the purposes of the 12-month holding rule.

To calculate the gross deemed gain/loss the capital proceeds will be determined based on either:

- the market value of the asset just prior to 1 July 2027; or

- where the taxpayer elects to apply the “apportionment method”, the capital proceeds calculated under that method.

At this stage, the draft legislation does not provide detail on how the apportionment method will operate. This is expected to be prescribed by the Minister through a legislative instrument, which has not yet been released.

We outline below how the different acquisition dates will impact the CGT implications based on the draft legislation.

1. Pre-CGT assets

All assets acquired before 20 September 1985 (known as pre CGT assets) will be brought into the CGT regime from 1 July 2027, regardless of the entity holding the asset. This represents a significant shift, as such assets have historically been excluded from capital gains tax. The gain or loss from acquisition to 30 June 2027 remains excluded from CGT. Any capital gains accruing after 1 July 2027 are subject to CGT under the proposed legislation.

The question many are asking is, should taxpayers obtain a valuation as at 1 July 2027? Currently the answer is difficult to provide as presently we have no details regarding the apportionment method. Further, this answer will need to consider each taxpayer’s individual circumstances.

2. Post-CGT assets purchased before 1 July 2027

Similar to pre-CGT assets, the deemed disposal from acquisition to 30 June 2027 will need to be understood. Any capital gain or loss arising on the deemed disposal of an existing asset is disregarded and deferred until the asset is ultimately realised by the taxpayer when the asset is sold. Importantly, it is the gain or loss on the deemed disposal that has access to the 50% discount or the pre-1999 indexation rules if the entity holding the asset is entitled to these based on current legislation. The post 1 July 2027 gain or loss will be calculated under the new cost base indexation method. As such, keeping records of any additional costs for the assets from 1 July 2027 will be important for this calculation.

The important question again for these assets remains around how to calculate the proceeds for the deemed sale. Waiting to understand the apportionment method is likely best practice, although personal circumstances may alter this.

3. Post 1 July 2027 assets

Assets purchased post 1 July 2027 will fit solely within the proposed rules. As such, cost base indexation will apply. For these assets, it will be important for the taxpayers to keep detailed records of the purchase costs and future additional costs to ensure the indexation calculation is able to be completed efficiently and effectively.

4. CGT asset acquired and disposed of before 1 July 2027

Capital gains and losses for this period will continue to be assessed under the existing legislation. Accordingly, the new regime will not apply to those gains or losses.

Minimum 30% tax rate on capital gains

The proposed legislation also introduces the minimum 30% tax rate on capital gains that are realised by individual taxpayers (or attributed to individual taxpayers as beneficiaries of trusts) on or after 1 July 2027.

Under the current regime, where an individual triggers a CGT event, any resulting capital gain is taxed at their applicable marginal tax rate. Under the proposed changes, however, individuals will be subject to a minimum tax rate of 30% on capital gains, irrespective of their overall income level.

A similar outcome is expected to apply to capital gains distributed from a trust to an individual beneficiary. That said, where a discretionary trust itself becomes subject to a 30% tax, it is likely that this liability would effectively satisfy the minimum tax requirement on capital distributions made to beneficiaries. We will be able to understand how the two different proposed changes interact once the draft legislation for the 30% tax on discretionary trusts is related.

Based on the 2026 financial year individual tax rates (including Medicare Levy), an Australian resident individual taxpayer with taxable income of $199,188 is subject to an average tax rate of 30%. Accordingly, where an Australian resident individual’s total taxable income, inclusive of any capital gain, is at least $199,188, the proposed 30% minimum tax on capital gains would be broadly neutral in its impact. However, where an Australian resident individual’s taxable income falls below $199,188, the application of the minimum 30% rate would result in a higher tax liability, leaving the taxpayer worse off under the proposed regime.

Broadly, the 30% minimum tax rate for capital gains will not apply in the following circumstances:

- Deferred gains on existing assets: Capital gains arising from the deemed disposal and re acquisition of existing capital assets will not be subject to the minimum tax, even where the assets are ultimately realised on or after 1 July 2027.

- Recipients of income support payments: Taxpayers assessed on capital gains who receive specified income support payments, such as the Age Pension, Disability Support Pension and JobSeeker, will be excluded. The precise list of excluded taxpayers under qualifying support payments will be prescribed through a legislative instrument later.

- New residential dwellings: The minimum tax rate will not apply where a taxpayer has elected to apply the CGT discount in respect of new residential dwellings or affordable housing, rather than adopting the indexation method. The definition for new residential dwellings will be prescribed through a legislative instrument later.

CGT examples: Comparing current vs proposed tax outcomes

To assist with understanding the application of the proposed CGT changes, we have calculated three scenarios highlighting the different capital asset acquisition dates and treatment under the proposed legislation.

Assume that there is an initial investment of $500,000, the indexation percentage is consistently 2.5% each year and the rate of return on the asset is 5.5% each year it is held. The asset was sold after a 10-year holding period.

| Net Capital Gain | Net tax payable comparison** | |||||

| Asset ownership period | Deemed disposal gain* | Cost base indexation gain | Total taxable gain | Current rules | Proposed rules | Difference – proposed less current |

| $ | $ | $ | $ | $ | $ | |

| 10 years up to 1 July 2027 | 137,500 | 137,500 | 34,963 | |||

| 5 years before 1 July 2027 & 5 years after | 68,750 | 69,375 | 138,125 | 35,207 | 34,988 | – 219 |

| 10 years after 1 July 2027 | 150,000 | 150,00 | 39,838 | 48,000 | 8,162 | |

* 50% discount applied

** Using 2026 tax rates, including Medicare Levy and 30% minimum tax on the gain post 1 July 2027

Who will be affected by CGT changes?

The proposed CGT reform will impact investors of all assets. From the family groups who hold investment properties to taxpayers who own and operate businesses.

The proposed 30% minimum tax on capital gains is expected to have the most significant impact on taxpayers’ after-tax returns, particularly for those who had planned to benefit from a lower marginal tax rate in retirement. However, it is also important not to underestimate the effects of transitioning from the current 50% discount method to a cost base indexation approach, as this change may materially alter the magnitude of capital gains tax payable.

The indexation method is likely to favour taxpayers holding long-term capital assets where returns do not significantly exceed the rate of inflation. By adjusting the cost base for inflation, this approach seeks to ensure that only the “real” gain is subject to tax. This differs from the 50% discount method, which was designed to simplify capital gains calculations and promote investment in long term capital assets.

Forward planning: What you should do now

The proposed changes have not yet been legislated. However, if you are considering the acquisition of a capital asset, it is prudent to factor in the potential impact of the proposed rules as part of your broader investment and financial planning strategy. Conversely, for existing asset holders, the reforms, once enacted, are likely to apply to you. Accordingly, once the legislation is finalised, it will be important to assess how these changes may affect your future plans and retirement savings outcomes.

Understanding the value of capital assets as at 1 July 2027, including any pre CGT assets, will be critical. Under the draft legislation, taxpayers are provided with two options to determine this value: a market value approach or the Government’s prescribed apportionment method.

Currently it is difficult to determine which option will be more favourable, given that the details of the apportionment method have not yet been released. As such, careful planning will be essential once further guidance is available. This will enable taxpayers and their advisers to assess both approaches based on their specific circumstances and optimise future tax outcomes.

Negative gearing changes: What property investors need to know

Proposed negative gearing rules: Key details

The draft legislation proposes that established residential properties acquired after 7.30pm AEST on 12 May 2026 will only be able to deduct the net rental losses against residential income or capital gains resulting from the sale of residential properties.

All residential properties acquired before that time will be fully grandfathered – meaning the owners can continue to access negative gearing benefits under the existing rules. Dwellings that are converted from a main residence into an income producing asset are also grandfathered. Additionally, the existing rules will continue to apply for real property interest in vacant residential land on which a residential dwelling is built on the land after 7.30pm (AEST) on 12 May 2026. This will also include land where a residential dwelling is being built or is contracted to be built, and the completion of construction occurs after this time.

The new measures will not apply to:

- New residential dwellings: The draft legislation does not define what constitutes a “new residential dwelling.” This will be determined by a legislative instrument later.

- Residential dwellings used for prescribed activities or enterprises: The prescribed activities/enterprise may be determined by a legislative instrument later.

- Residential dwellings owned by widely held unit trusts or superannuation funds.

Who is affected and how to plan your property investments

Future property investors are going to be among those most affected by the proposed changes. We recommend that investors carefully consider how the proposed negative gearing reforms may impact their individual circumstances and investment objectives.

Where possible, it may be prudent to defer property investment decisions until the legislation has been enacted, unless there is an immediate intention to invest. In this context, ensuring the appropriate structure is in place for residential property investments will become increasingly important under the proposed regime.

Discretionary trust tax changes: Will a 30% tax apply to your structure?

Proposed 30% tax on discretionary trusts: What has been announced

The Labor Government are looking to make discretionary trusts a thing of the past with the introduction of a 30% non-refundable tax on distributions. From 1 July 2028, the proposed changes will see 30% tax paid on distributions paid by the trustees and passed to the beneficiaries, although it will not be refundable to the beneficiary.

We expect draft legislation for the taxation of discretionary trusts to be released later this year. For now, we only have the guidance that was provided to us on Budget night. For our summary of the proposed rules, please see here.

Who will be affected by trust tax changes?

While we understand that the Government are targeting wealthier groups, owner-managed businesses who operate though a discretionary trust will bear the brunt of these changes. Additionally, if you have a discretionary trust that distributes to any of the following, these rules will impact your family group structure:

- Not for profits that are not deductible gift recipients;

- Individuals with taxable income of less than $200,000;

- Companies; or

- Another trust.

The Budget papers indicated that the proposed 30% minimum tax rules capture discretionary testamentary trusts that are not in existence as at 7.30pm AEST on 12 May 2026. As such, those with discretionary testamentary trusts in their Wills should be considering these when they are enacted.

Forward planning: What to do before July 2028

Taxpayers are currently reviewing their structures to understand how the proposed rules will impact them personally. Although this is a good starting point, we caution making changes too soon, particularly given we have no legislation in place as yet. Further, based on the Government’s current record changes are likely to occur – to what extent we will need to wait and see.

The Government has announced it will introduce a time limited (3 years) restructure rollover with the discretionary trust 30% tax measure, commencing 1 July 2027. Details on this rollover are currently unknown, although it’s likely to defer Federal taxes that may be payable – due to a change in the operating structure – but not State taxes. Where this is the case, a restructure from a discretionary trust will likely bring an upfront cost at the time the rollover is applied.

Discretionary trusts have provided many benefits to family groups. Trusts are usually the go-to entity when family groups are looking to purchase investment assets or start a business. They have been excellent entities for investments and business as they provide:

- Asset protection;

- Distribution flexibility;

- Opaqueness of ownership; and

- Tax minimisation strategies.

Should the proposed introduction of the 30% tax on discretionary trusts be enacted, taxpayers will need to weigh up what is more important out of the above list, together with how they utilise their trust. Post the introduction of these changes (being 1 July 2028) it’s likely one structure will not provide all of the above benefits that family groups are currently receiving.

For some, the advantages of holding a discretionary trust may outweigh the disadvantage of a minimum 30% tax rate. As this is a case-by-case basis, you should decide what you want to prioritise in your structure before making any major decisions.

While we await the release of draft (preferably final) legislation, taxpayers should begin considering how the proposed changes may impact their existing family group structures. This is particularly relevant for those holding investments through discretionary trusts, including interests in privately owned companies.

For individuals considering the use of a discretionary trust as part of their business or investment structure, and where there is no immediate commercial need, it may be prudent to defer implementation until further details are released. This will allow for a more informed assessment of the available options, as well as the associated advantages and disadvantages under the proposed regime.

On the other hand, for individuals looking to transact now, who don’t have the luxury of waiting, we recommend reaching out to your Pilot advisor to assist you with understanding the structuring options and risks, and to provide you with the details you need to make an informed decision.

Contact Pilot

If you would like assistance with your tax planning or have questions regarding any of the above Federal Budget measures and how they might impact you, contact Kylee Smith or your Pilot advisor on (07) 3023 1300.

Latest Federal Budget News

Pilot Partners’ taxation advisory team will continue to keep you up to date on the tax consequences related to the Federal Budget and how they will impact your business.